Learn more about new Google Wallet updates, including new ways to use your digital ID for age and identity verification.

Learn more about new Google Wallet updates, including new ways to use your digital ID for age and identity verification.

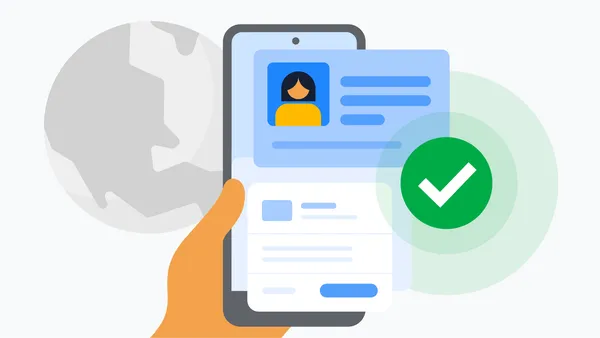

It’s now easier to prove age and identity with Google Wallet

Learn more about new Google Wallet updates, including new ways to use your digital ID for age and identity verification.

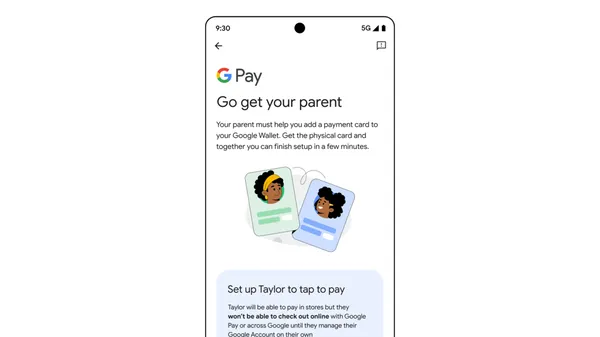

Google Wallet now gives parents and guardians in the U.S., U.K., Australia, Spain and Poland a way to allow their children to access digital payments on their Android de…

Google Wallet now gives parents and guardians in the U.S., U.K., Australia, Spain and Poland a way to allow their children to access digital payments on their Android de…

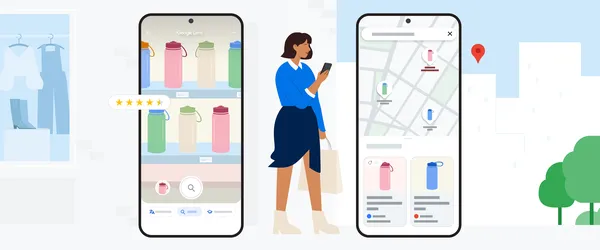

Learn more about new Google Lens, Shopping and Pay updates, available for shoppers this holiday season.

Learn more about new Google Lens, Shopping and Pay updates, available for shoppers this holiday season.

Check out Google Wallet’s new type of digital ID as well as new transit features.

Check out Google Wallet’s new type of digital ID as well as new transit features.

Keep up with the 2024 Paralympics across Search, Maps, YouTube, Google TV and more.

Keep up with the 2024 Paralympics across Search, Maps, YouTube, Google TV and more.

Keep up with the 2024 Olympics across Search, Maps, Gemini, YouTube, Google TV and more.

Keep up with the 2024 Olympics across Search, Maps, Gemini, YouTube, Google TV and more.

We’re breaking down device tokens: what they are, how they work and why they make digital payments safer.

We’re breaking down device tokens: what they are, how they work and why they make digital payments safer.

We’re making online checkout even easier with three features.

We’re making online checkout even easier with three features.

For Financial Literacy Month, we’re sharing a few ways Google Pay keeps your digital payment information safe.

For Financial Literacy Month, we’re sharing a few ways Google Pay keeps your digital payment information safe.